How fast is Europe’s battery storage market really growing – and can deployment keep pace with the accelerating energy transition?

Answers come from the latest edition of the “European Market Outlook for Battery Storage 2026–2030”, published by SolarPower Europe on June 24 at The smarter E Europe 2026.

The annual report examines the most important developments in the European battery storage sector and provides in-depth insights into key market segments, including utility-scale storage, commercial and industrial applications, and residential battery systems. The full report is available free of charge on The smarter E Digital . This article summarizes the key forecasts, trends and market developments.

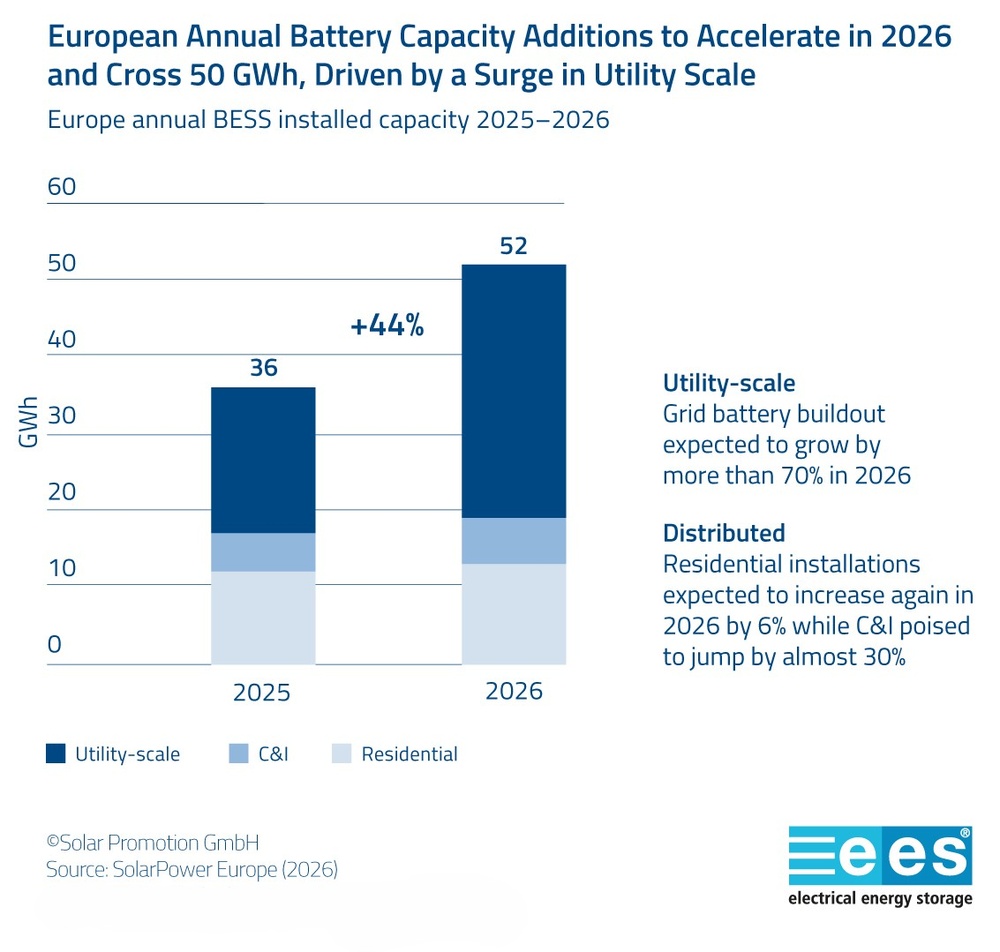

Europe’s battery storage market experienced a sharp acceleration in 2025, with annual installations increasing by 48 percent to 36 GWh. The increase of 11.7 GWh compared with 2024 marks the largest year-on-year capacity gain ever recorded in the European market. Since 2022, annual installations have more than tripled, highlighting the industry’s strong recovery after a period of slower growth in 2024.

The EU accounted for 27 GWh of new capacity, which equals three-quarters of all battery installations across Europe. Despite ongoing policy uncertainty, battery deployment continued to exceed expectations. Investment activity remained strong as well, with European BESS investments reaching €17 billion in 2025, a 20 percent increase from the previous year.

Utility-scale projects emerged as the key growth engine in 2025. Installed capacity in this segment rose to 19 GWh, almost double the 9.7 GWh recorded in 2024, and represented more than half of all new battery installations. Another comparison: Europe now adds ten times more utility-scale battery capacity than it did in 2021 and around 40 times more than in 2019.

Distributed storage regains momentum, while utility-scale growth reshapes the market

Alongside the boom in utility-scale storage, Europe’s distributed battery storage market returned to growth in 2025. Residential and commercial users installed 16 percent more battery capacity than in 2024, which reversed the slight decline recorded the previous year.

The residential segment recovered modestly, with installations rising 3 percent year-on-year to 12.3 GWh, which is equivalent to more than 1.5 million battery systems. Since 2020, nearly 5.4 million European households have adopted solar-plus-storage solutions. But within the EU, residential battery installations continued to decline, falling by 7 percent in 2025 after an 11 percent drop in 2024. Limited support schemes, resistance from grid operators and lower retail electricity prices remain key barriers to wider adoption of household storage.

Commercial and industrial (C&I) storage systems emerged in 2025 as another strong growth area. Installations surged by 77 percent to 4.7 GWh, raising the segment’s share of annual deployments to a record 13 percent. The increase reflects a growing number of businesses that combine on-site solar generation with battery storage to maximise self-consumption and reduce peak electricity costs.

Europe’s cumulative battery storage capacity exceeded 100 GWh in 2025, an increase of 55 percent compared with the previous year. The market continues to expand at an exceptional pace: installed capacity has grown tenfold since 2021 and is now 100 times larger than in 2016. Despite reaching this milestone, the sector remains firmly in a phase of rapid growth.

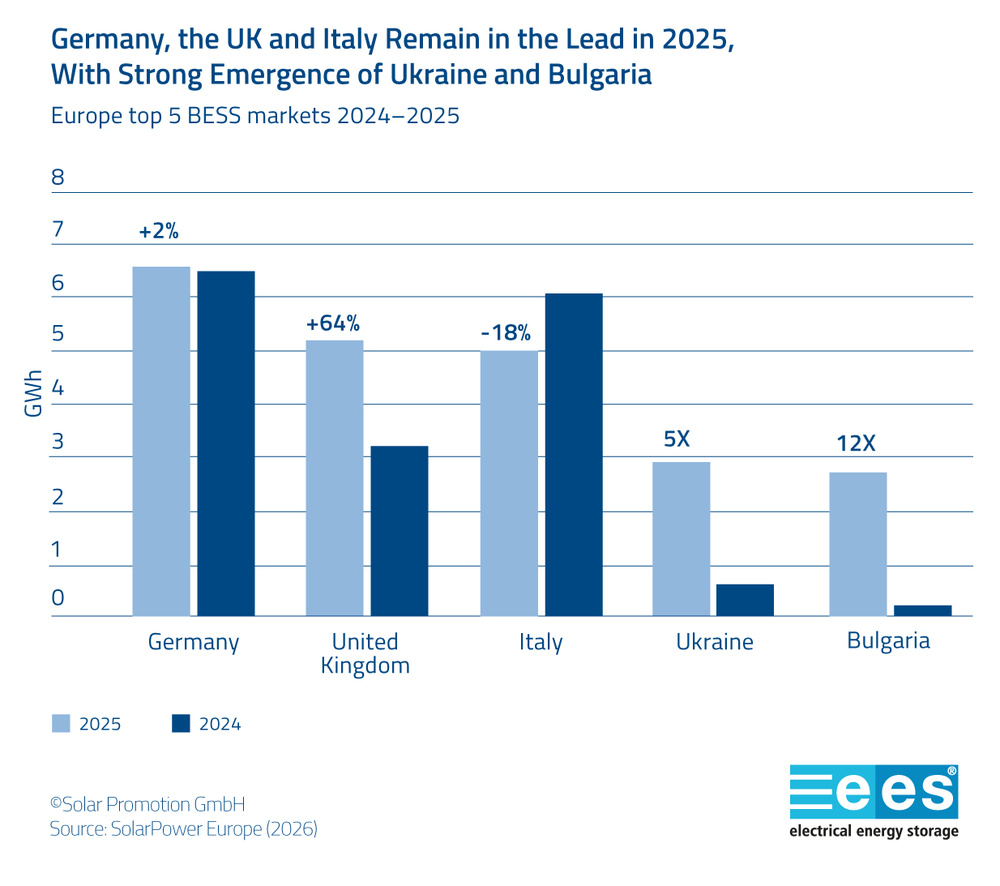

Together, these five countries accounted for 62 percent of all battery storage installations in Europe in 2025, although the market is becoming more diversified as more countries deploy battery storage at scale.

While residential solar markets slowed in 2024 and 2025 as electricity prices stabilised and support schemes became less attractive, battery attachment rates continued to rise. Across Europe’s mature markets, nearly 40 percent of new residential solar installations were paired with batteries in 2025, indicating that solar-plus-storage has become the preferred choice for many households.

Countries such as the Netherlands and Poland illustrate the importance of regulation: In those countries, generous net-metering schemes initially encouraged solar adoption without significant battery deployment. As these schemes were gradually phased out and dedicated battery incentives introduced, battery attachment rates climbed rapidly, surpassing 50 percent in 2025.

The C&I segment has lagged behind the residential market. Although businesses installed more than 80 GW of solar capacity between 2022 and 2025, battery adoption remained comparatively low, with attachment rates generally below 5 to 10 percent. As a result, Europe’s C&I solar fleet is roughly 27 times larger than its associated battery capacity.

Nevertheless, battery uptake among businesses has begun to accelerate. By 2026, attachment rates had increased to around 20 percent in the commercial sector and 10 percent in the industrial sector, signalling a gradual but growing integration of storage alongside on-site solar generation.

- Antonio Arruebo, Senior Market Analyst at SolarPower Europe, on the growth of the C&I segment and the importance of solar-plus-storage for businesses:

Drivers for utility-scale battery deployment

Growing volatility in Europe’s wholesale electricity markets has emerged as a key driver of utility-scale battery storage deployment. As renewable energy capacity expands, batteries play an increasingly important role by exploiting price spreads, delivering balancing services and enhancing grid flexibility. These capabilities significantly improve project economics.

A key indicator of this trend is the increase in negative electricity prices, which rose from less than 0.5 percent of the year before 2022 to 3.4 percent in 2025, reflecting periods of high solar generation and insufficient system flexibility. At the same time, intraday price spreads have widened significantly and led to greater revenue opportunities for battery operators.

The strongest increases in price volatility have been observed in markets such as Germany, Poland and Spain, where renewable deployment has outpaced flexibility resources. In Germany, average intraday spreads have nearly tripled since 2017 to 2018, highlighting the growing value of battery storage in balancing the power system. By contrast, volatility has risen more moderately in France, where nuclear generation provides greater system stability, and in the UK, where a relatively large battery fleet already helps smooth market fluctuations.

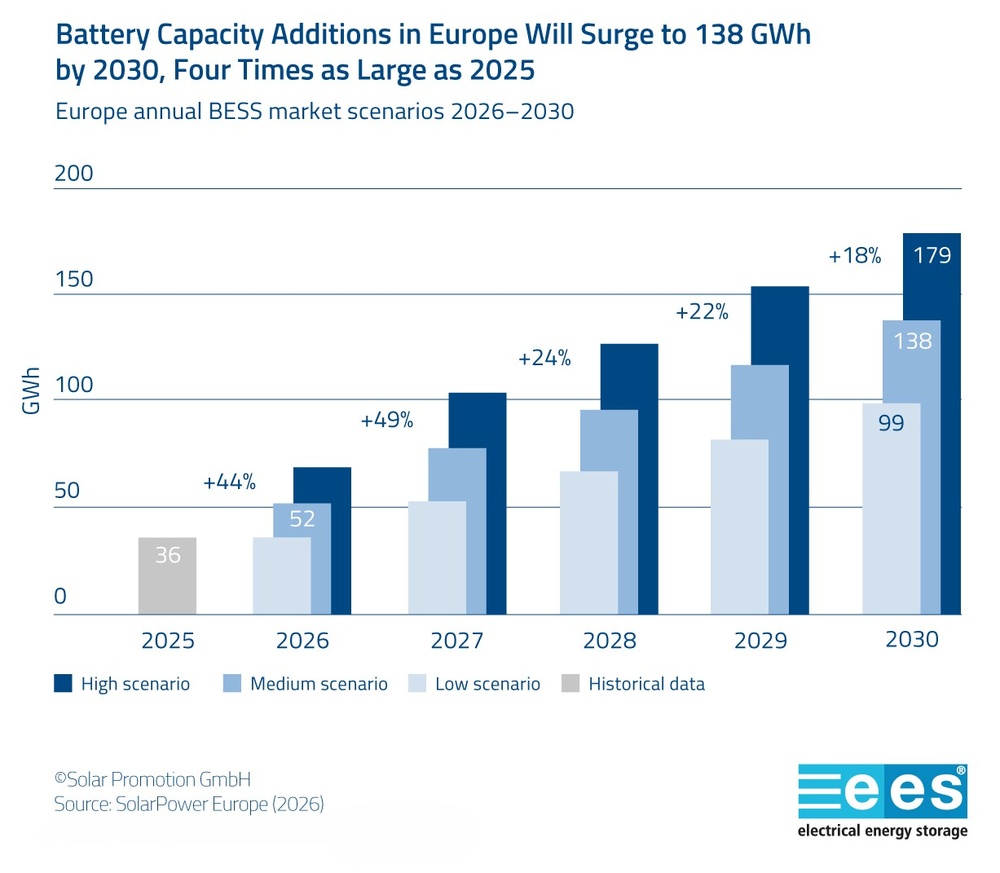

Europe’s battery storage market is expected to continue its rapid expansion throughout the decade. Under the report’s medium scenario, annual installations will surpass 50 GWh in 2026 and grow to almost 140 GWh by 2030, while cumulative installed capacity is projected to exceed 580 GWh. Even in the low scenario, annual deployments are expected to reach nearly 100 GWh by 2030, while the high scenario points to around 70 GWh already in 2026 and approximately 180 GWh annually by 2030.

Utility-scale batteries will remain the main growth engine. Their share of annual installations is forecast to rise from 53 percent in 2025 to 63 percent in 2026, driven by more flexibility needs, improving project economics, falling technology costs and strong investor interest. By contrast, distributed storage will continue to grow more gradually.

In the residential segment, installations are expected to increase by 7 percent to 13.2 GWh in 2026, supported by dynamic tariffs, lower solar export remuneration and a higher demand for energy independence. The C&I segment is projected to expand even faster, growing 26 percent to 5.9 GWh, as businesses increasingly adopt solar-plus-storage systems to lower energy costs and improve resilience.

Despite the positive outlook, the report highlights persistent challenges, including grid connection bottlenecks, lengthy permitting procedures, regulatory uncertainty and limited access to revenue streams. According to industry estimates, the EU would require at least 600 GWh of battery storage capacity by 2030 to support a highly renewable and electrified energy system. Under current assumptions, only the optimistic scenario comes close to achieving that level.

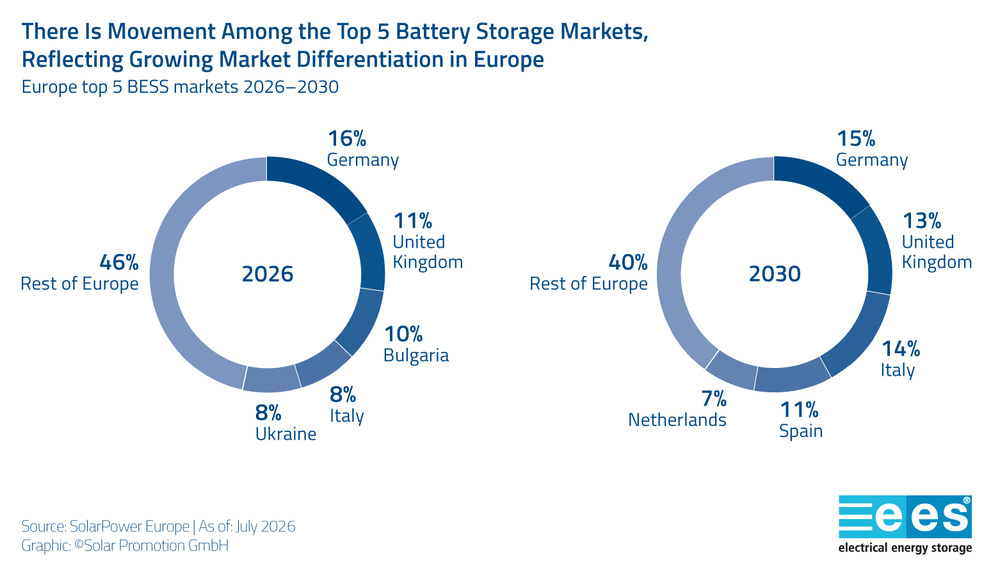

Europe’s battery storage market is expected to become more diversified in the coming years, with a growing share of installations that occur outside the traditional leading markets.

Markets such as the Netherlands, Spain, Austria, Belgium, Greece, Poland and Romania are expected to be among the strongest contributors to this trend. Regulatory reforms, storage auctions, support programmes and streamlined permitting procedures are helping accelerate deployment. Notably, Greece has launched multiple storage auctions and approved significant grid-scale battery capacity, while Romania is projected to double its market size for a second consecutive year.

By 2030, however, Germany, the UK and Italy are forecast to remain Europe’s three leading battery markets, while Spain and the Netherlands are expected to join them in the top five rankings for annual installations.