What is driving the growth of the battery storage market – and what is no longer relevant? Which applications and trends are shaping the sector today, and what can we learn from battery storage developments in countries like the UK?

As part of the Drivers for an Accelerated Deployment of Battery Storage Systems in Europe auf der ees Europe Conference 2025 session at the ees Europe Conference 2025, Antonio Arruebo, Market Analyst at SolarPower Europe, explored the key factors that have influenced the market over the past few years and presented an outlook for the next five years. One thing is certain – battery storage remains a fast-evolving sector.

The presentation highlighted insights from the “European Market Outlook for Battery Storage 2025-2029”, which is available after the login for free download from our on-demand platform, The smarter E Digital.

Future expansion of solar PV and associated challenges

To understand the necessity of increased BESS deployment, it is important to provide an overview of the current challenges associated with the energy transition. According to the “Global Market Outlook for Solar Power 2025-2029”, nearly 600 gigawatts of solar PV capacity were installed worldwide in 2024. The EU deployed around 340 gigawatts of solar in the same year. Looking ahead, REPowerEU, a renewable energy project implemented by the European Commission, envisions 750 gigawatts of solar PV capacity by the year 2030 for Europe.

“While this goal appears achievable under a medium-growth scenario,” explains Arruebo, “our forecasts have been repeatedly downgraded over the past year. This is primarily due to the growing challenges associated with the energy transition, especially integrating increasing amounts of solar PV into the grid.” Many EU member states are already facing significant difficulties. On the one hand, there are technical challenges, such as grid integration issues and rising curtailment levels. On the other, there are also financial challenges, including inefficiencies caused by the market structure, reduced investment attractiveness, and concerns over the remuneration of renewable energy producers.

To ensure a smoother energy transition, Europe must address curtailment, negative electricity prices, and solar price cannibalization with an increased deployment of BESS. Battery storage can reduce curtailment by absorbing surplus solar and wind energy that would otherwise be wasted. It mitigates negative electricity prices by balancing the grid in real time, preventing supply from drastically outpacing demand. In short, battery storages are essential to unlocking the full potential of renewables while maintaining grid stability and economic efficiency.

The BESS market is already experiencing a shift from a market for home owners to one that is increasingly dominated by large-scale solar and storage projects. A crucial factor for the adoption of residential systems was the availability of financial support schemes across Europe, which generally fall into two categories: CAPEX subsidies and tax incentives.

“For the new European Market Outlook for Battery Storage,” Arruebo continues, “we mapped the current status of these schemes across the EU and found that support remains fragmented, inconsistent, and largely insufficient. This is especially problematic given the current market dynamics, where electricity prices have stabilized and some countries are even phasing out financial incentives, which is further slowing residential adoption. Companies often lack sufficient financial support, especially where funding gaps exist. Addressing this would significantly boost technology adoption in the commercial sector.”

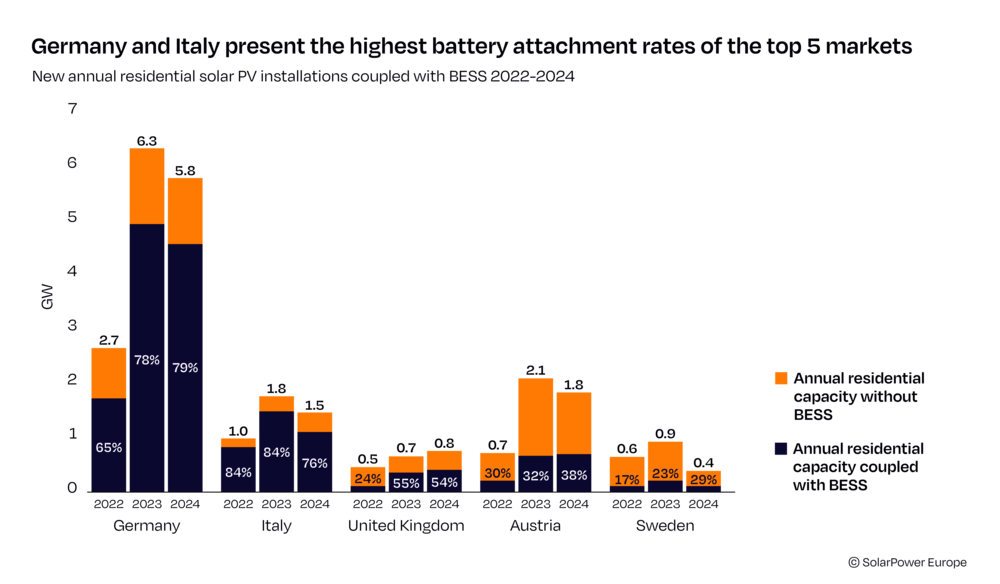

While the number of residential PV and battery installations surged during the 2022 – 2023 energy crisis, with average attachment rates (percentage of solar PV installations that also include a battery storage system) in the EU reaching around 80 percent, the commercial and industrial (C&I) segment lagged behind. Battery attachment rates for C&I remained below 5 percent across the EU, among other things because companies installed a lot of PV, but not as many batteries.

This poses a problem for the industry’s decarbonization goals, given that companies can only achieve 20 to 30 percent self-sufficiency rates with a standalone PV system. Batteries could make businesses more independent from the grid, reduce peak demand charges, help phase out diesel back-up systems, and reduce their operations’ carbon footprint. Additionally, these hybrid systems can provide essential grid balancing and ancillary services, thus improving the grid’s flexibility and resilience.

Unless frameworks are improved at the residential and C&I levels, we will not see significant market recovery, and most of the capacity will be delivered by grid batteries.

Drivers for grid battery deployment

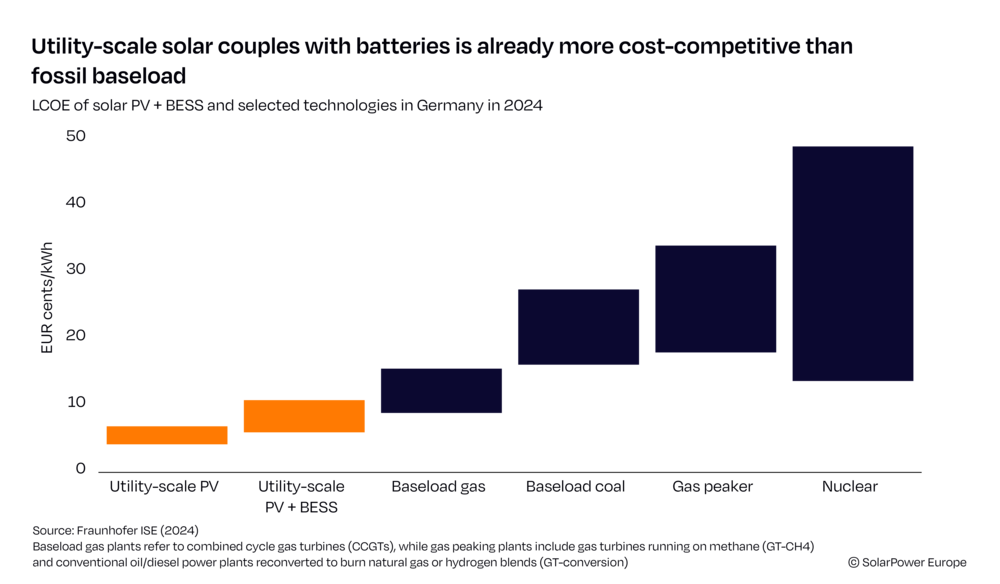

When it comes to the deployment of utility-scale battery storage, one focus of interest is cost competitiveness with fossil-based baseload generation. A 2023 Fraunhofer study compared the Levelized Cost of Electricity (LCOE) of newly constructed solar PV with utility-scale battery storage and other new energy technologies in Germany. The results show that utility-scale PV with storage is significantly cheaper – the LCOE (in euro cents/kWh) is 45 percent below that of baseload gas, 160 percent lower than that of coal, over 200 percent lower than that of gas peaking plants, and even 377 percent lower than that of nuclear power. In 2024, the LCOE for PV and battery storage were even lower.

Although these promising findings could serve as a clear impetus for further expanding renewable energies, most National Energy and Climate Plans (NECPs) still lack detailed strategies for grid investment, flexibility, and digitalization. Only 14 European countries have set quantitative energy storage targets, but many of these targets remain unambitious and are not aligned with the flexibility needed to support future deployment. Moreover, of these 14 countries that have set energy storage targets, only nine, such as the UK and Spain, have specific targets for battery storage.

Another key driver of utility-scale battery deployment is revenue stackability – the ability of a battery to generate income from multiple value streams by providing different services. “Our review of the European member states found that, while more revenue streams for battery storage have opened over the past year, many grid services remain unpaid – meaning batteries are often providing these services without compensation,” says Arruebo. Since many grid services are bundled or cannot be procured separately, it is difficult to monetize specific capabilities fully, thereby lowering the remuneration on essential grid services.

Among the available revenue streams, fast frequency regulation is the most accessible, with 19 out of 29 countries offering it. Balancing and restoration services are available in 14 countries, while only eight have developed broader ancillary service markets. Only Germany, Portugal, Spain, and the UK offer all three main revenue streams.

When it comes to capacity markets – which compensate battery systems for their availability to support the grid during peak demand periods, even if they are not dispatched – only seven countries allow the participation of battery systems in the capacity market. “Participation is a complex procedure that is now being discussed in many countries as we transition to a more complex and intermittent energy system that requires reserve capacity,” Arruebo adds.

Another key market development is the hybridization of solar and storage. As Arruebo mentions in his presentation, the bankability of solar projects is increasingly at risk, and pairing them with batteries is a key solution for existing and future installations.

In 2024, batteries boosted the market value of solar electricity by on average 18 percentage points across four major European markets – Germany, Spain, Hungary, and the Netherlands. However, hybrid systems remain limited. Currently, only about 5 percent of the battery storage fleet is paired with solar, either as fully integrated hybrids or co-located systems, which represent just 1,1 GWh of capacity. In contrast, over 19 percent of the fleet operates as standalone storage, highlighting the significant untapped potential for solar-storage hybridization.