Are power grids ready to support the demands of the energy transition? This is one central question, DNV answers in its most recent “Industry Insights – Future-proofing our power grids – Research Report". We asked Ditlev Engel, CEO of Energy Systems at DNV, about the findings of the report and the big challenges involved in transforming the power grid to suit a new energy mix.

What are the most important findings from your "Industry Insights – Future-proofing our power grids – Research Report "?

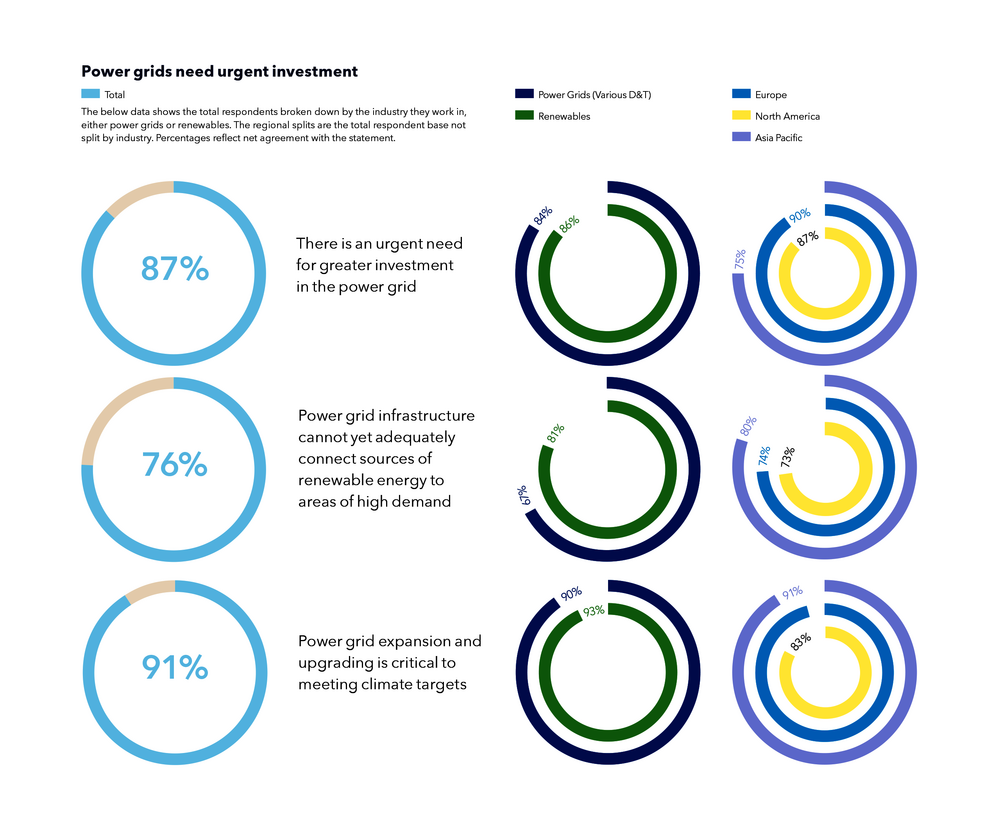

We are entering a new paradigm and the industry must transition faster to a more electrified and deeply decarbonized energy system. Unlike the smaller iterative changes implemented in the past, future-proofing our grids calls for a thorough transformation of our energy system: according to our latest Energy Transition Outlook, power grids investment needs to grow by 50% in the next ten years, to secure reliable distribution, meet climate targets, achieve energy security, and better connect regions.

Our research shows that three quarters (76%) of the 400 senior energy professionals surveyed believe that grid infrastructure as it exists today can’t adequately connect renewable energies to areas of high demand, and over nine-in-ten (91%) say that expanding and upgrading power grids is critical to meeting climate targets. Most consider the highest priority for the energy transition to be grid capacity expansion, especially in Europe.

What are the most important trends in the expansion and modernization of the power grids? And what role do digital solutions play in this?

Our survey identified some key priorities for future-proofing our power grids and the majority were linked to digitalization, including improving data quality and availability, making better use of automation and improving cybersecurity. As the energy transition advances, grid operators will need to rely more on digital tools to manage and operate generation, transmission, and distribution assets in real time, to be able to properly balance electricity supply and demand. However, many grid operators are currently juggling the demand to future-proof whilst keeping the day-to-day operations running... Upgrading aging/legacy infrastructure was the second most cited priority by T&D operators today (67%), after grid capacity expansion.

Some energy experts say there is a tipping point at which the power grid will no longer be able to cope with the growing demands caused by the expansion of renewables, and power outages will increasingly occur. What are your thoughts on this?

Fortunately, there are many existing mitigations that can be taken by grid owners and -operators before unplanned outages may occur. Also digitalization and new technologies offer additional means to provide resilience and secure availability of the grid. Yet this does imply that these should be designed, implemented and managed while monitoring the growth of demand and generation on all power levels in the grid, from connecting offshore wind on high voltage networks to EV on low voltage networks.

Because improving and upgrading the grid may take longer than connecting RES and electrification, local discrepancies may result in dis-balance, congestion and stress on the existing asset base, which may result in curtailment, increased number of planned outages and eventually failure rates. The rapid electrification of domestic and commercial appliances, transport and industry, will increase the impact of these on society in general. Communication and alignment between all systems’ stakeholders is therefore a key.

What are the biggest barriers to grid modernization in Europe?

In Europe, as well as globally, the biggest barriers for power grids are both socio-political and technical. Lack of policy support was cited by 49% of our survey respondents, closely followed by the capacity constraints of existing grid infrastructure (42%). Overcoming the latter may be prevented by the former, as well as the third-and fourth-ranked barriers, respectively: difficulties in securing permits or licenses (42%), and public objections or resistance (32%). Lesser concerns also include human resources issues (skills shortages and/or aging workforce, at 29%). Difficulties in securing permits or licenses, in particular, are more frequently cited as a concern in Europe than in any other region. Public resistance is also higher in Europe than anywhere else, though the contrast is less marked.

What role do supply bottlenecks play today and in the future for the modernization and expansion of the grid?

Inadequate supply chain capacity was cited as a top-three barrier to a faster energy transition by 18% of respondents overall. This was significantly higher (29%) in North America, where there is significant concern about a lack of domestic manufacturing capabilities. The limited availability of materials will put even greater strain on supply chains, which are already under great stress due to multiple factors, including geopolitical issues and the continuing changes created by the pandemic. Current models anticipate that the electricity sector will need about twice as much copper, aluminium and steel in 2050 as it did in 2015; that will drive up prices, but also require clear and far-reaching directions about producers’ and operators’ responsibilities in terms of circularity and re-use of materials.

In your study, you state that there are still many unanswered questions about what the energy system of the future will look like. In this context, how important are international events like The smarter E Europe, where the entire energy industry comes together to discuss precisely these questions?

Industry events do provide a great opportunity for the players to gather together to exchange ideas and new concepts, which we can hopefully put into practice. DNV is always emphasising more collaboration across the industry to accelerate the energy transition.

Do you want to receive monthly updates on recently published interviews, best practices and industry news? Then sign up for the EM-Power Newsletter!

Subscribe to the EM-Power-Newsletter